SEEDING A NATION'S FUTURE

What is the greatest thing you can do today to ensure your wealth for tomorrow? Plant a seed today. Imagine a nation that enthuses individuals to adventure into enterprise, building the future in accordance to their imagination – and subsequently funding that adventurous spirit. And what shall we call the funding of that adventurous spirit? Why not Seed Funding? Today on “The Other Side with Sihle Sibeko” we are making the call to action – a call to unleashing South Africa’s adventurous spirit for enterprise through venture capital!

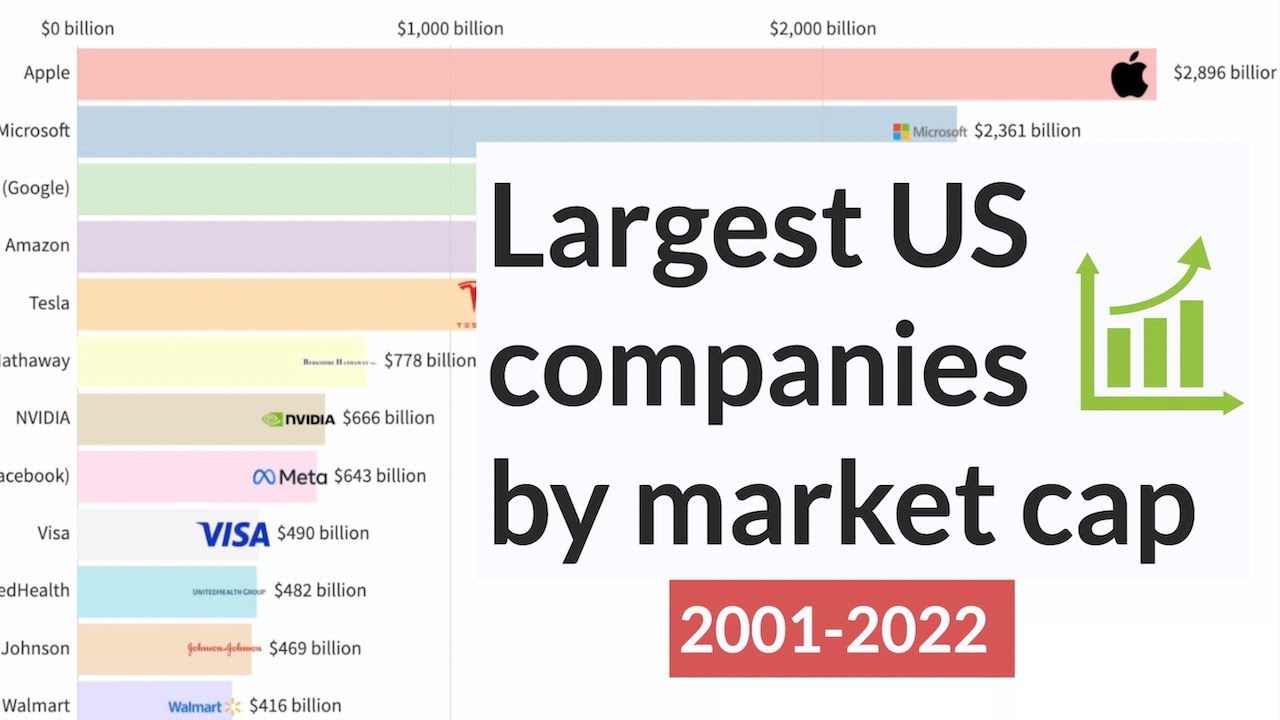

By the end of Q1 in 2000, the largest listed companies (even dual-listed) in the USA by market cap were the following

1) General Electric; 2) Cisco; 3) Intel; 4) Microsoft; 5) Exxon Mobil; 6) Walmart; 7) Citigroup; 8) Royal Dutch Shell; 9) Vodafone; 10) IBM; 11) Pfizer; 12) AIG; 13) BP; 14) Toyota; 15) Merck…

By Q3 2022, the 15 largest are below:

1) Apple; 2) Microsoft; 3) Alphabet; 4) Amazon; 5) Tesla; 6) Berkeshire Hathaway; 7) UnitedHealth; 8) Johnson & Johnson; 9) Exxon Mobil; 10) Visa; 11) Walmart; 12) Meta; 13) Chevron; 14) JP Morgan Chase; T15) Eli Lilly, Nvidia, AbbVie; Bank of America

Within 30 years, only 3 of the 15 companies in the first list are present on the second list. Incredibly so, the total market cap of the 15 combined was $3.927 trillion, fast forward to 2022 and the combined market cap of Apple and Microsoft alone ($4.01 trillion) is worth more than the entire first list, in fact Berkshire Hathaway’s (#6 on the list) largest investment holding is Apple which accounts for 45% of their portfolio. Add to boot, 7 of the companies in the second list were founded after 1990. That is the power of innovation, advancement and propulsion of an entrepreneurial spirit as a national ideal in a growing economy. This phenomenon of the industrial juggernauts being replaced by new-age tech hubs is not restricted to USA either – just ask Singapore, China, Great Britain and New Zealand about it.

This brings us to South Africa – where 24 of the JSE’s Top40 companies in 2000 remain on the list in 2022. Yes the JSE was the best performing exchange for the 20th century and into the 21st, but that was driven by the countries commodity advantages & cheap labour afforded by egregious Apartheid laws. Gone are those day, and now South Africa MUST innovate or be left behind. South Africa’s private markets industry is still nascent, albeit burgeoning, with the South African Venture Capital Association representing a collective of over R205 billion in assets. Still, more must be done – particularly in venture capital and innovation.

So what are things RSA must do to establish a more competitive Venture Capital industry?

1. CLEAR THE ROADMAP

South Africa’s private markets industry is still quite fractured. Take a peek into more developed private markets – there is a consistent roadmap for growth. A company launches from angel funding, to pre-seeding funding, to seeding, to initial venture capital, to series-based rounds to eventually IPO, trade sale or private equity. In South Africa, the intersection of angel to venture to IPO is not so clear-cut, and in fact it is very unlikely for a venture investee to reach full maturity of IPO exit potential. This turns venture investments, which are time-capped to a maximum of 10 years of holding, into principal investments, which have no exit directives upon investment. This trend is largely driven by:

- An outweighing of generalist funds vs specialist funds, whereby the generalist fund makes investments into a multitude of companies at different stages in their growth cycles with no clear fund strategy;

- A lack of investee education in sequencing their business life cycle to the different stages of funding required;

- Lack of collaboration between investors at different funding stages (although this is now getting a lot better).

If South Africa’s private markets industry is to garner a venture capital market that will give rise to a slew of future corporate behemoths and innovators, then that roadmap must be clearly designed and defined to eventuate a new class of entrepreneurs turned corporate titans.

2. INSTITUTIONALIZED!!!!

For long, venture capital, particularly in South Africa, was much maligned by institutional investors with serious risk aversion because “there is so much risk” or “we can’t control the outcomes or risk” or “how do you know this is going to work” – but if you had invested $500 000 in Peter Thiel’s “Founder’s Fund” in 2005, the year Thiel’s fund invested into $META, you would’ve seen an over 2800x return on your capital – ballooning $500 000 to just over $1.4 billion. Or what about KCPB, the VC that invested in $AMZN – what if you invested $500 000 in them? Well, that’s a 3130x return on capital; a sweet $1.56 billion. Whilst these are the outliers, venture capital is all about the marksmanship of its general partners; a 1.45x – 2.2x DPI (Distributions-to-Paid-In) return is the industry standard for a new venture capital firm’s first fund in San Francisco, with an expected fund lifetime of 6 years. That’s an impressive 18.9% - 27.23% year-on-year return until realization. If South African venture capitalists apply a same return metric, that would far outstrip JSE’s 12% return over the past five years – which is actually a real return of 3%, further negated by the fact that the equity market risk premium for South Africa is closer to 4%.

Institutional investors must also realize that investing in venture capital is deployment of capital into the real economy. These are investments into the innovative companies that will create new jobs, new industries, and new infrastructures - spurring competitors to also innovate. Such investments have seismic shifts on a nation’s competitiveness over the long-term. While the attitude towards venture capital among institutional investors is changing, (uptrend in new managers, greater capital flows, more deal activity due to increased capital allocations), the narrative must be accelerated that deploying funds to venture capital is not only spurring a burgeoning asset class with greater influx of diverse managers, it is also a patriotic act of the highest order.

3. BUMP THE CHEESE UP!

Recently a certain company published that they received a capital injection from a venture capital company and are looking to expand their service offering into the continent. Excitable as I was reading the article, it all dissipated soon as I read the investee received R10 million. If you can show me a company that has expanded into Africa with R10 million (less whatever is used in sustaining current operations), I’ll bite my arm off.

South Africa’s venture capital injections must also be measured up to standard. In South Africa, a certain fund manager raised a $6.4 million fund as a follow-on to their initial fund. Two weeks later, two start-ups in Nigeria raised a combined $6.9 million in pre-seed funding, a third start-up raised $8 million in seed funding and an Egyptian fintech raised a $120 million pre-series B round the week after that. Sure one could point to population density and market size, but South Africa is still Africa’s most diversified economy and has the highest GDP per capita for countries with a population greater than 2.8 million. If South Africa is serious about competing in Africa’s great venture capital gold-rush, then the funds raised and equity cheques must be indicative of our economic might and desire to produce the next generation of this continent’s business powerhouses.

Investors, both limited partners and general partners, must understand that backing a strong entrepreneur with big dreams is going to require significant amounts of capital for those dreams to be realized. More than that they will need investors who understand that mistakes are a pivotal part of the process in building a business. Whereas as in Singapore, USA and China VC's make provisions for first loss, second loss and even third-losses for their investees, South Africa tends to shy away from this – expecting perfect performance with the capital afforded or face eternal excommunication from any future capital flows. I hope South African investors will allow more latitude for the entrepreneur to grow from their mistakes and create positive feedback loops from them – because in most instances, if INDEED the entrepreneur is truly as strong as the VC believes they are, then it won’t come to a point of third-loss provisions.

If South Africa wants to see great venture successes and greater capital flows from even international financiers, then the country must seriously bootstrap its venture capital ecosystem – that is the consciousness I hope every leaves this post with.

Siyabonga!

This week's affirmation: I am seeding my future with blessings, prosperity and abundance

This week's vibe: https://open.spotify.com/track/1Yd7meWF4xNR13vys5IpUh / https://www.youtube.com/watch?v=w0sWGh95jeU / https://music.apple.com/us/music-video/what-do-you-say-move-it-baby/1541083817 - What Do You Say by Common feat PJ | https://open.spotify.com/track/6ezLjo6aPEaN6KlCCvYvyd / https://www.youtube.com/watch?v=NwIyiNITT1A / https://music.apple.com/us/song/1342240697 - It's Complicated Pt.2 by Thandi Ntuli

Enjoying the content? Follow me for more:

LinkedIn: https://www.linkedin.com/in/sihle-sibeko-095a0488/

Twitter: https://twitter.com/TheSihleSibeko